Tweet

Tweet

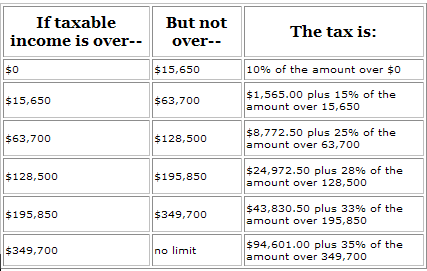

I know cross-posting isn't allowed but this in the other thread was getting a bit fuddled with other things and I want to attract some of our more economics savvy posters on this topic. I kind of feel like I'm doing something wrong but it's making sense to me logically.

Now, Kuciwalker was trying to make the point that a Capital Gains tax is unfair because it increases the effective tax rate for investors. I agree with this but same that taketh can giveth, it seems. Check it:

Now, Kuciwalker was trying to make the point that a Capital Gains tax is unfair because it increases the effective tax rate for investors. I agree with this but same that taketh can giveth, it seems. Check it:

Originally posted by Albert Speer

View Post

Comment